On Foundation Markets

The first wave of automated market makers (AMMs) are having a moment. From Uniswap to Balancer to Curve, these protocols have amassed billions in liquidity and consumed mindshare in equal proportion. But it turns out that the creation of automated and programmable markets are good for more than just financial assets. Foundation represents a new class of AMM designed for ecommerce.

Foundation is a marketplace for creators to sell limited-edition goods like clothing and art. It diverges in structure from Uniswap and the like where markets are optimized for decentralized liquidity. Different assets require different design choices. On Foundation, markets are optimized to work for creators. Foundation Markets are owned by GPs, the creators themselves, rather than LPs, a community of liquidity providers. No up-front capital is required to bootstrap a market. And price curves are fully determined from the outset.

Monetizing hype.

Collections sold on Foundation are limited-edition, deriving value from an artificial supply cap like Yeezys… or Bitcoin. Flat rate pricing leaves money on the table in this case. The last unit of a collection is worth and should be priced substantially higher than the first unit. Creators can now set a starting price, ending price, and the slope at which price ramps up.

Price curves inevitably attract speculators. Historically, speculation was problematic given that creators don’t get a cut of the resale value while end buyers get up charged. Creators and speculators don’t have to be at odds, though. On Foundation, markets are programmed to distribute a fee to creators on every resale. Speculative trading serves as an additional income stream for creators. For the first time, creators can monetize their hype.

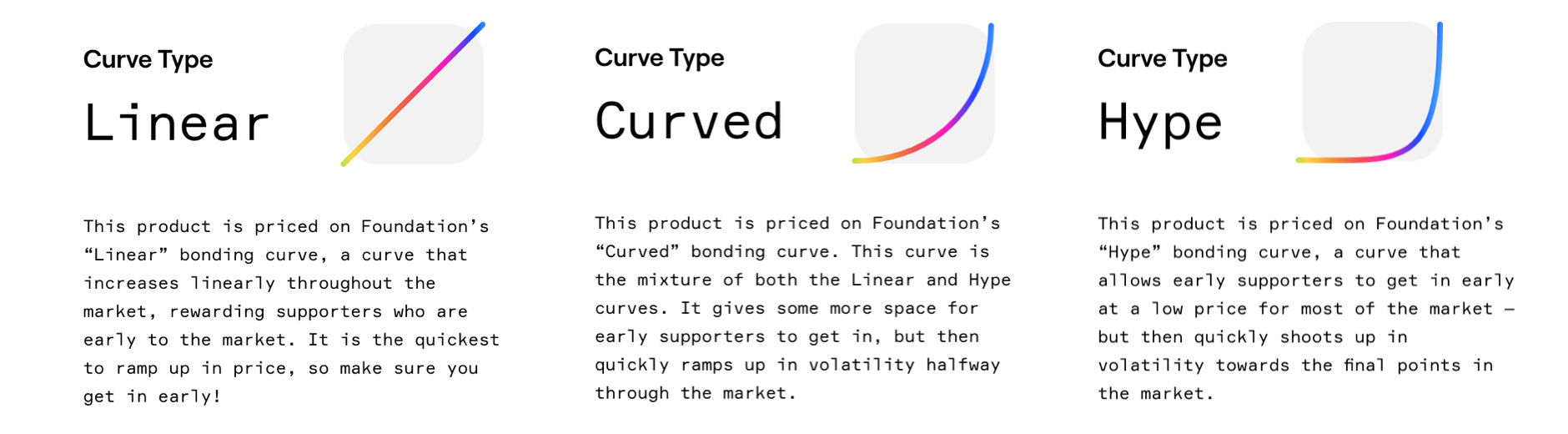

How fast and how far price should rise is more an art than a science. Foundation offers several templates, each with their own tradeoffs between giving space for supporters by suppressing prices and fueling speculation by ramping up prices more quickly.

You would never otherwise design for this behavior in a creator-owned marketplace. You would never otherwise incentivize early buyers to flip a piece of your collection for speculative gain. Or a fraction of a piece in your collection. Half a sock, let’s say. But Foundation is able to lean into secondary markets, making trading commonplace for a much wider set of goods than previously imaginable.

Tertiary markets, or how things get weird.

Ok, now take this a step further. Consider the second-order effects of programmable markets in a composable ecosystem. We already have the first independently run data service built atop Foundation, a Bloomberg style terminal for creator markets. The sorts of yield seeking instruments built to speculate on financial markets are equally composable with ecommerce.

Derivatives can increase exposure to individual collections. Indices can offer exposure to categories of collections so you can go long the price of all traded merch or concert tickets not just a single one. Liquidity mining can allow creators to juice their returns while earning an ownership stake in the network, like Rarible has done. Each of these tools heightens trading activity and generates further income for creators. If secondary markets monetize hype, tertiary markets let them moon.

Something perhaps more subtle happens when all of this income is captured on-chain. Bringing limited edition collections on-chain inevitably brings the creators on-chain too. Derivatives can go long just a creator’s collection or all of a creator’s on-chain income across their current and future markets. You can potentially get exposure to up-and-coming artists, brands, and makers who plan to launch many collections. Personal tokens and DAOs with measurable on-chain cash flows fit nicely into this ecosystem.

Foundation isn’t coy about this future for their platform. They’ve hinted at liquidity mining already. And, after all, they refer to themselves as “culture’s stock exchange.” Doesn’t the realization of such a vision include exotic financial instruments? Or maybe a better question is how much more accessible do crypto’s yield seeking tools become when applied to sneaker drops instead of protocol tokens?

Super interesting, where do I find out more?